By the end of this section, you'll be able to:

- Open a vehicle record and start an HP or Conditional sale finance report

- Enter the agreement details correctly so the figures reflect reality

- Review the finance tracker, equity, and settlement breakdown

- Apply the right interest period when validating settlement estimates

- Record actual settlement figures and build up a settlement history

- Use the financial projection to plan against liability and market value

Step 1: Open the vehicle record and find the finance section

- Select the relevant vehicle record on the Vehicles page.

- Go to the Vehicle Data page by clicking on the relevant registration number.

- Scroll down to the Financial Overview section.

- Confirm you're working on the correct vehicle before generating the report.

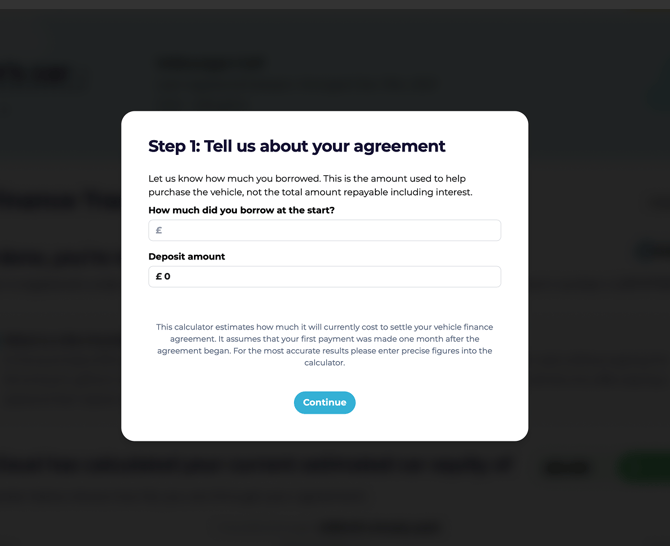

Step 2: Start the report and enter the initial finance details

- Click Generate Report.

- In the pop-up, confirm Yes if the vehicle is financed.

- Enter the vehicle's monthly payment.

- Enter the vehicle's current cumulative mileage.

- Enter the estimated annual mileage for this vehicle.

- Click Continue to let the platform identify the agreement type.

Step 3: Complete the HP or Conditional sale agreement questions

- Once the borrowing and deposit details are input correctly, click Continue.

- The platform will display the agreement summary.

- Review the valuations shown — the platform will generate an estimated settlement figure based on the information you've entered.

💡 Have your agreement documents to hand before starting. Deposit is easy to mis-remember.

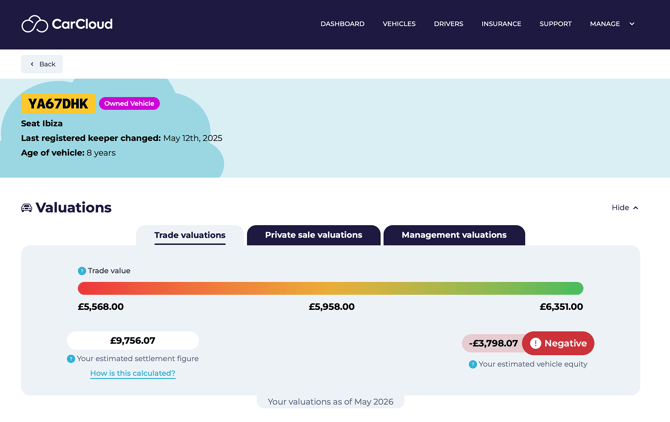

Step 4: Review the report summary and valuation outputs

-

- Review the report once it loads.

- Check the valuation sections:

- Trade valuation

- Private sale valuation

- Management valuation

- Locate the estimated settlement figure.

- Review the estimated car equity shown against the settlement figure.

Step 5: Inspect the Finance Tracker for agreement details

- Scroll to the Finance Tracker section.

- Confirm the vehicle is listed under an HP or Conditional sale agreement.

- Verify the provider name and agreement number.

- Read the agreement description to understand the HP or Conditional sale structure.

- Review the agreement details populated from your inputs, including:

- Monthly vehicle repayment

- Total amount borrowed

- Monthly interest

- Daily interest

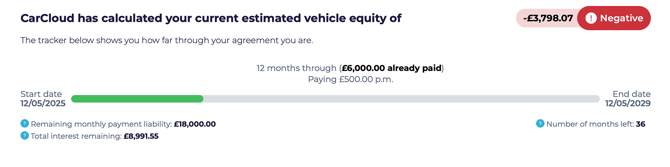

Step 6: Check repayment progress and remaining liability

- Review how far through the agreement the vehicle is.

- Check how much has already been paid based on the monthly payment you entered.

- Review the remaining figures shown:

- Remaining monthly payment liability

- Total interest remaining

- Number of months left

⚠️ Missed payments aren't included in the calculation. If the account isn't fully up to date for payments, treat the figures as a guide rather than a precise position.

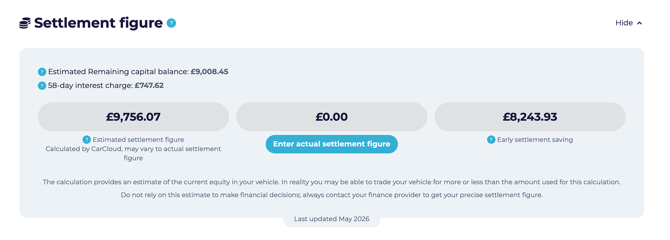

Step 7: Review the settlement figure and early settlement saving

Savings opportunity! It is often possible to settle the agreement early by paying a settlement amount consisting of the outstanding capital plus a smaller amount of interest. But this may only be possible once 50% of the finance agreement has been paid up (see Voluntary Termination section).

- Locate the Settlement Figure section.

- Review how the estimated settlement figure was calculated.

- 58-day interest charge is automatically applied if your agreement length is longer than 12 months. If the agreement length is 12 months or shorter a 28-day interest charge will be automatically applied.

- Check the early settlement saving displayed alongside the settlement figure.

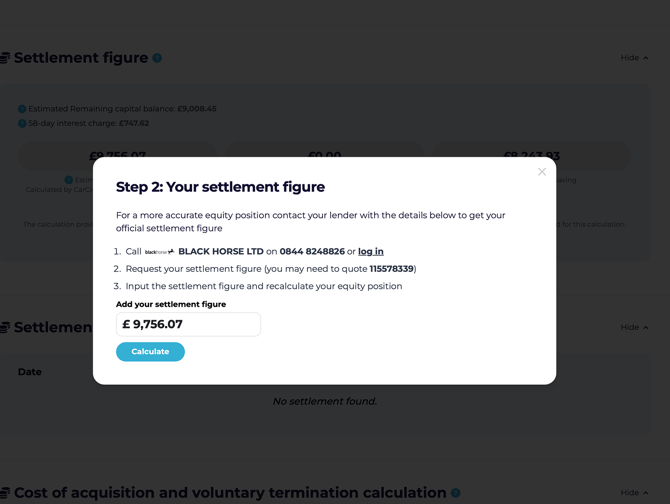

Step 8: Enter an actual settlement figure when you have one

- If you have the actual settlement figure from your agreement documentation, click Enter Actual Settlement Figure.

- Enter the value in the pop-up.

- Click Calculate.

- Confirm the estimated settlement figure greys out and the actual settlement figure becomes the active value.

⚠️ Only enter an actual settlement figure once you've verified it with the lender. Settlement values change monthly, so always use the most current information available.

Step 9: Recalculate equity and review settlement history

- Review Step 10: Review voluntary termination and acquisition calculations section.

- Use this section to determine whether voluntary termination is possible.

- Assess whether the outcome would result in a shortfall or surplus based on the agreement.

⚠️ Voluntary termination outcomes vary by agreement. Always check for a potential shortfall or surplus before making any decision based on these figures.

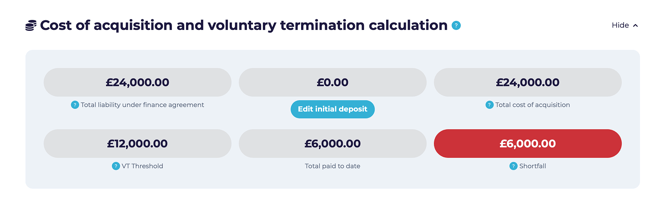

Step 10: Review voluntary termination and acquisition calculations

- Scroll down to the Cost of Acquisition and Voluntary Termination section.

- Review the figures shown against the VT threshold.

- Identify any shortfall or surplus based on the calculation.

- Use this section to assess whether the agreement is approaching voluntary termination limits.

⚠️ Voluntary termination outcomes vary by agreement. Always confirm the shortfall or surplus before making a decision based on these figures.

Tips for keeping finance reports accurate

- Have the original agreement documents to hand before starting so you can quickly enter the borrowed amount, deposit, and agreement number.

- Use the estimated settlement figure first if the actual figure isn't immediately available, then refresh it once you have the real number.

- Re-run the report monthly to keep settlement and equity information current.

- Use the six-month projection to support timing decisions without needing separate manual calculations.

What's next?

- Head to Loan Vehicle Finance Reports or Lease and Contract Hire Finance Reports or PCP finance reports if you also manage vehicles on those agreements.

- Visit the Vehicles Management page to review the wider vehicle record.